representing company / license with

FIMM: The Federation of Investment Managers Malaysia (FIMM) is a self-regulatory organisation (SRO) that regulates the marketing and distribution of Unit Trust Schemes (UTS) and Private Retirement Schemes (PRS).

Unit Trust Scheme(UTS)

with

Phillip Mutual Berhad

Private Retirement Scheme(PRS)

with

AHAM Asset Management Berhad

- Group Financial Consultant with Phillip Mutual Bhd

- FIMM UTS certification 1999

- FIMM UTS number 043-0-23182

- UTS since 1992

- Prior with Pacific Mutual Fund Berhad (now known as BOS Wealth Management Berhad) since 1994

- started with Kuala Lumpur Mutual Fund Berhad(now known as Public Mutual Berhad)on 1992

- Group Manager with AHAM Asset Management Berhad

- FIMM PRS certification 2013

- FIMM PRS P-038-0-20315

- PRS Since: 2013

Strategy / Investment Plan Available

Lumpsum Plan

- One off,

- Top-up anytime

- Monthly Investment

- Autodebit bank account

- A sure win long-term strategy

KWSP-MIS Plan

- Capitalize on long-term

- KWSP Calculator

investment method

Financial Literacy

Nominal Rate Vs Effective Rate

Master Your Freedom by Understanding the Difference

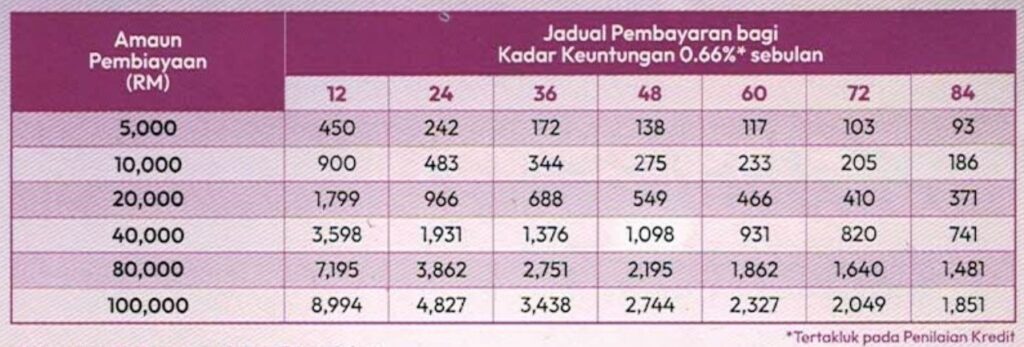

How Most People Calculate Loans: Nominal Rate

- $450 \times 12 \text{ months} = \$5,400$ (Total Repayment)

- $\$5,400 – \$5,000 = \$400$ (Total Interest)

- $(\$400 / \$5,000) \times 100 = \mathbf{8\%}$ (Interest Rate)

How Finance instituition Calculate Loans: Effective Rate

Using a Financial Calculator (e.g., HP10Bii) or Time Value of Money (TVM) formulas, set to 12 payments per year:

The Core Formula:

FV = PV(1 + i)n

(Where FV is Future Value, PV is Present Value, i is interest, and n is time)

Calculation Inputs:

PV (Present Value): 5,000

PMT (Monthly Payment): -450

FV (Future Value): 0

N (Periods): 1 (year)

Result (I/YR): 14.54

Food for Thought

The bank does indeed use an 8% figure in their marketing, but because most people don’t understand the Time Value of Money (TVM), they end up effectively paying 14.54%.

It’s not a matter of “fairness”—it’s that banks have no obligation to educate you. It is your responsibility to master the math behind your money.

Contact me to learn more! Trust Fund Group Consultant | Making Money Work for You

“You don’t know what you don’t know; you only know what you know.”

財商教育

名義利率(Nominal Rate) Vs 實際利率(Effective Rate)

掌控自由從了解名義利率和實際利率的分别開始。

一般人的借貸算法:名義利率(Nominal Rate)

- $450Ⅹ12月=$5400=還款總數

- 5400-5000=400=利息總額

- 400/5000×100=8%=利率

金融的借貸算法:實際利率(Effective Rate)

*1 用金融计算机(HP10Bii)或科學計算机機(本人不用)

*2 金融計算機設置一年12次還款

- 時間金錢價值的方程式: 未來 = 現值(1+利率)年數

- 計算: 5000=PV, -450=PMT, 0=FV, 1=N

- 答案:【I/YR】= 14.54%

思考: 銀行的确以8%計算,因为你不懂時間金錢價值的算法, 所以你付出14.54%。不是合不合理,而是銀行没有義務教育你,而是你不会時間金錢價值的算法。

聨络我了解更多! 讓金錢为你工作的信托基金组組織顧問。

【你不知道你不知道的,你知道你所知道的】Calvin Kho Ming Soon